It happens all the time. The Federal Reserve makes a monetary policy move (either raises or lowers the Fed Funds Rate) and folks expect mortgage rates to move in lock step, especially when that move is DOWN. Well, that’s not how it works. In fact, you might be shocked to know that after the Fed cut rates by 50bps on Wednesday, the popular 30yr mortgage rate actually ticked higher! How in the world is that possible and who benefits from this 50bps interest rate reduction anyway? Let’s dive in.

As Housingwire astutely points out: “The 10-year yield and 30-year mortgage rates have been in a slow dance since 1971 and trended together. The bond market isn’t old and slow like the Fed — it moves very quickly, and for months it has been sending the 10-year yield (and mortgage rates) lower in anticipation of a series of Fed rate cuts, not just one or two.

The above is important to keep in mind because the 10yr Treasury bond yield basically dictates mortgage rates. Let’s take a look at the bond yield action over the last six months. As you can see in the chart below, since the peak in April at 4.7390%, yields have fallen 113bps to 3.6040 on 9/18 (the day of the Fed meeting). But since the Fed lowered rates, bond yields have actually moved up to 3.7550 as of today; a small increase of around 15bps. To be sure, that is a signal the bond market had fully priced in a 50bp cut in rates, well ahead of the actual Federal Reserve announcement.

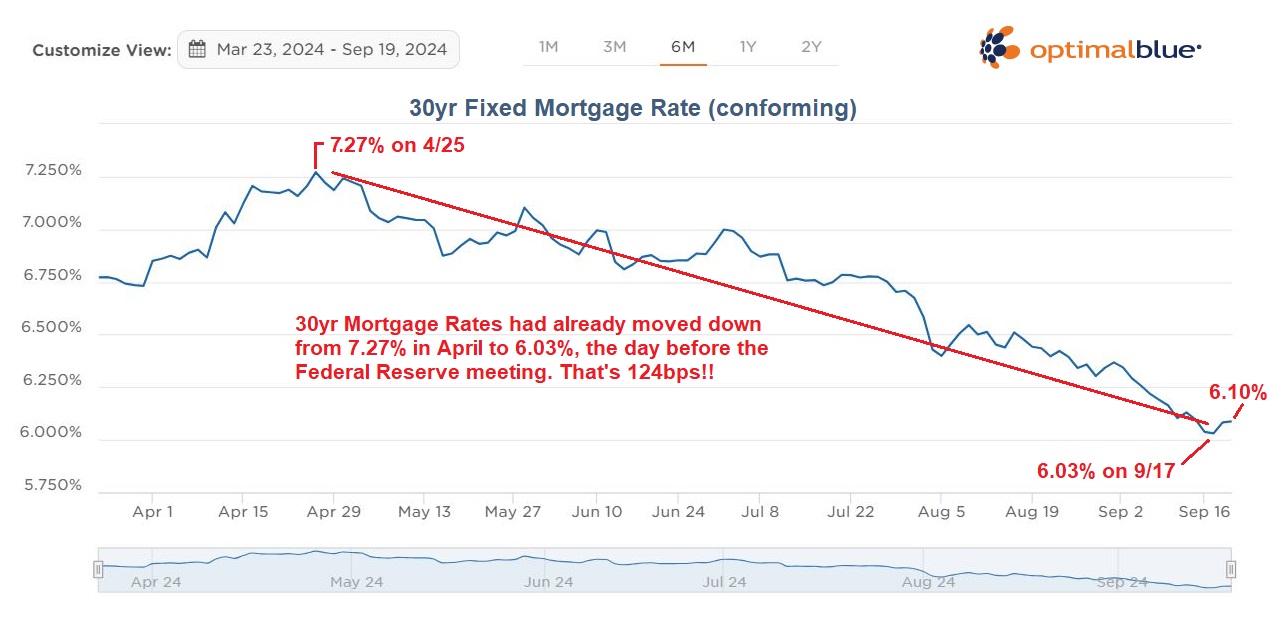

Let’s now look at the 30yr average fixed rate mortgage over that same period of time. Note in the chart below how mortgage rates were at 7.27% back in April, the same time that 10yr yields topped out. Since then, mortgage rates moved down to nearly 6%, just ahead of the Fed’s policy announcement. That’s 124bps (a bigger move than the bond market)!! So, after the Fed announcement, mortgage rates actually ticked up a bit. This should come as no surprise since the market has already priced in a series of official rate cuts.

The mighty bond market has a long history of pricing in Federal Reserve events way before they happen. Nothing has changed in that arena. If you’re a prospective homebuyer who is trying to time the market, don’t make incorrect assumptions about how future rate cuts will affect mortgage rates. The fact of the matter is that 30-year money around 6% isn’t too shabby, historically speaking, and expectations for drastically lower mortgage rates just are not in the cards at the moment. If you’re a recent homeowner who locked a rate in the 7’s or 8’s you might want to explore refinancing options now. The bottom line is that while official rate cuts can influence the economy, they have a more indirect influence on mortgage rates.

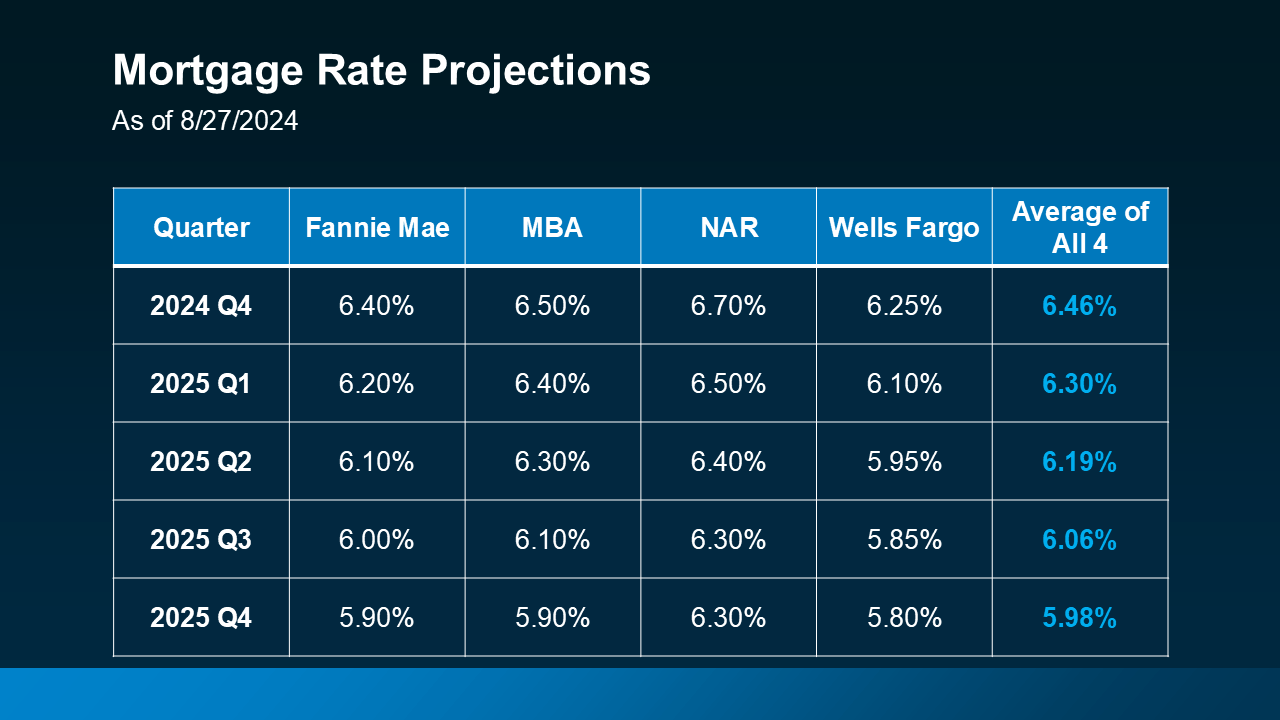

Now let’s take a look at the most recent expert projections for mortgage rates in the moths ahead. While this data was released before the Federal Reserve rate cut, all else remaining equal, we should not see much deviation form these longer-term projections. The one factor that could influence these projections is a possible recession, but let’s not get ahead of ourselves.

As you can see in the table below, all the respondents are projecting a very slow decrease in mortgage rates thru Q4 2025.

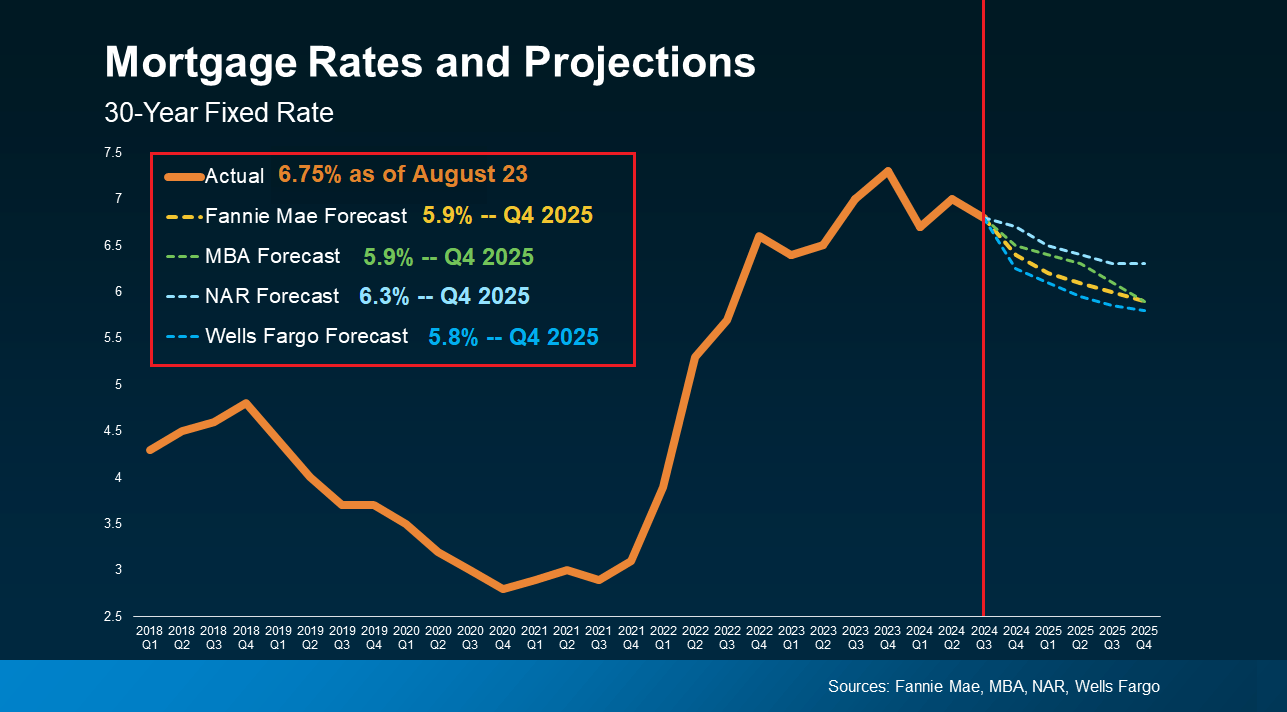

Here’s a graphical representation of the projections. Notice the very minor downward slope. Don’t hold your breath for repeat of Pandemic interest rates like we saw in 2020/2021. That’s not happening again anytime soon….possibly not ever again.

So who immediately benefits from Wednesday’s 1/2% rate cut? Well, consumers and businesses with loans tied to the prime rate, such as adjustable-rate mortgages, credit lines, and some credit cards, will see lower interest payments. This reduces borrowing costs and increases disposable income for individuals and profit margins for businesses. Take HELOCs for example: A Home Equity Line Of Credit (HELOC) is a variable rate revolving home loan that is tied to PRIME. Those folks just got a 1/2% interest rate reduction and there are more cuts on the way….great news for them!

Questions? Please feel free to reach out at your convenience!