I recently read an article on CNBC about rising home values, increasing property tax & insurance costs, and the fact that some would-be homebuyers are seeing the true cost of homeownership rise faster than their incomes. To be sure, the massive inflation spike that emerged during and after Covid has many questioning whether homeownership is still worth it. Let’s take a look at the numbers and discuss what prospective homeowners can do to better prepare themselves.

According to Harvard’s Joint Center for Housing Studies a record 20 million homeowners are considered cost burdened by their monthly payments, meaning they spend more than 30% of their income on housing costs. Homeowners are also facing a sharp increase in insurance premiums, up an average 21% between 2022 and 2023, according to the HJCH report, and property taxes are also rising.

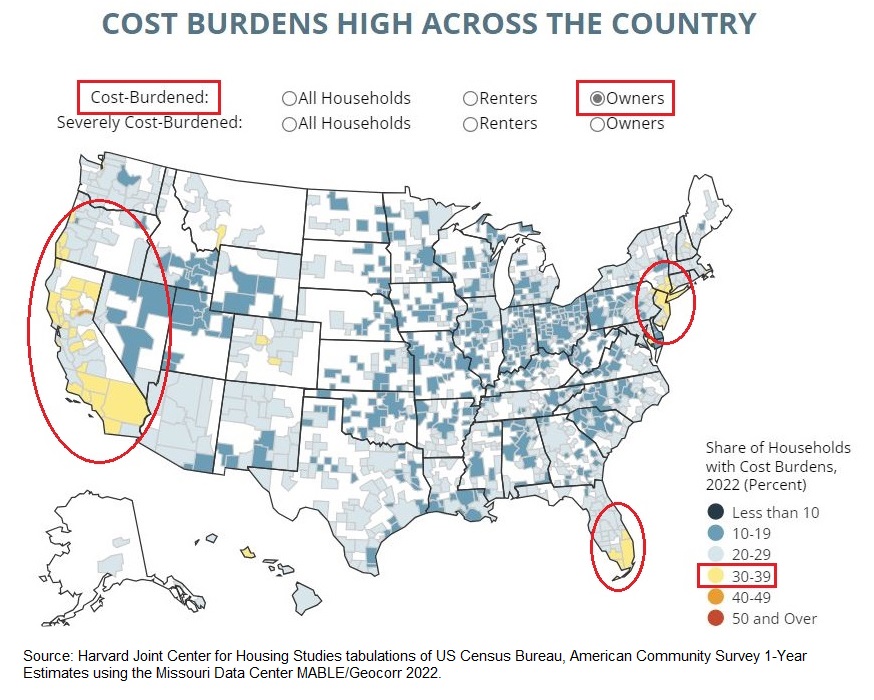

With data through 2022, you can see the national share of households with cost burdens in the graphic below. Unsurprisingly, some geographies on the East & West coasts have an alarmingly high percentage of cost-burdened homeowners — between 30-39%. In the Midwest it’s roughly 25%. Given the current state of the economy, it’s highly unlikely we’ve seen any improvement since the data were collected in 2022.

Interactive map link HERE.

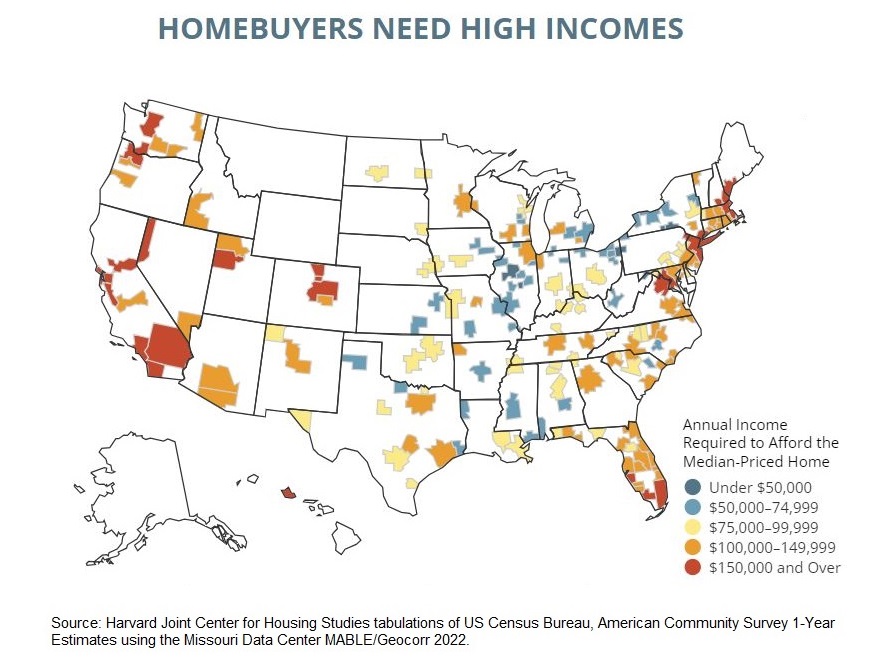

Using the same dataset, here is a national snapshot of the annual income needed to afford a median-priced home.

Interactive map link HERE.

Unfortunately, a lot of homebuyers enter into the mortgage borrowing process, but don’t understand that their monthly payment could change in the future. It’s not just being able to afford the Principal + Interest (P&I) of the loan, but also the “T&I” (Taxes + Insurance), or cumulatively, PITI. If you’re buying a condo or other property with a homeowners association (HOA), you also have to deal with Assessments. This is something to consider carefully and plan for ahead of time.

Mark Hamrick, senior economic analyst at Bankrate has this to say: “What many [homeowners] have failed to anticipate is the rise in both property taxes — and that’s correlated to the rise in the value of their home, something that at some level helps them — as well as the increased cost of paying for insurance.”

TAXES:

Homeowners whose properties were reassessed between 2019 and 2023 amid skyrocketing valuations saw a median tax increase of 25%, according to a February 2024 study by CoreLogic. The annual median taxes for properties in the U.S. that were reassessed increased more than $600 over that period.

INSURANCE:

Keep in mind that the cost of repairing a home has increased. This has helped to push insurance premiums higher. There has been a 20% increase in average home insurance premiums between 2021 and 2023, according to insurance comparison company Insurify. Insurify estimates rates will rise another 6% by the end of 2024. Florida, Louisiana, Texas and Colorado have seen the biggest spike in insurance rates over that period, influenced by extreme weather events.

Tips for prospective homebuyers:

- Know your geography and lean on your Realtor for advice. Property tax, insurance, trash removal, water, gas, and electrical bill history is valuable info that can help you plan your home budget.

- Plan for increasing expenses by leaving room in your monthly budget. Devon Viehman, regional vice president for the National Association of Realtors says: “Just because you qualify for $3,000 a month in a mortgage payment doesn’t mean you should max it out right now. Look for something where you can get in around $2,500 if $3,000 is your comfortable budget. Go a little lower than that so that you give yourself that room.”

- Your friendly neighborhood mortgage loan officer can help you plan as well. Have them run different scenarios with higher T&I figures so you don’t get any ugly surprises a few years after you close on your dream home.

Tips for current homeowners:

Current homeowners who are struggling to meet their monthly payments also have some options to consider.

- The Consumer Financial Protection Bureau recommends reaching out to the Department of Housing and Urban Development, to see if you qualify for any programs or additional help.

- The CFPB also suggests cash-strapped homeowners call their mortgage servicer to explain the situation: Why they’re unable to pay, whether it’s a permanent or temporary situation and details about their income and expenses. A mortgage lender may be able to work out a repayment plan or provide a loan modification.

- Be an educated consumer. Periodically shop for better insurance rates and keep tabs on what your neighbors are paying on their property taxes. Perhaps you’re entitled to a property tax appeal and you don’t even know it.

Being a homeowner is more expensive than ever, but some prudent financial planning can help alleviate problems down the road and help you realize the American dream of homeownership. When you’re ready to take the dive, please reach out! 😊👍