If you’re a prospective homebuyer, you’re probably fed up with high interest rates and ever increasing home prices. You might be asking yourself if it’s worth it to wait for a home price retracement, a recession, or even a housing market crash….like what happened in 2008-2009. Well, don’t hold your breath for another crash because the data isn’t supporting anything remotely close. Let’s take a look at some of the data in more detail.

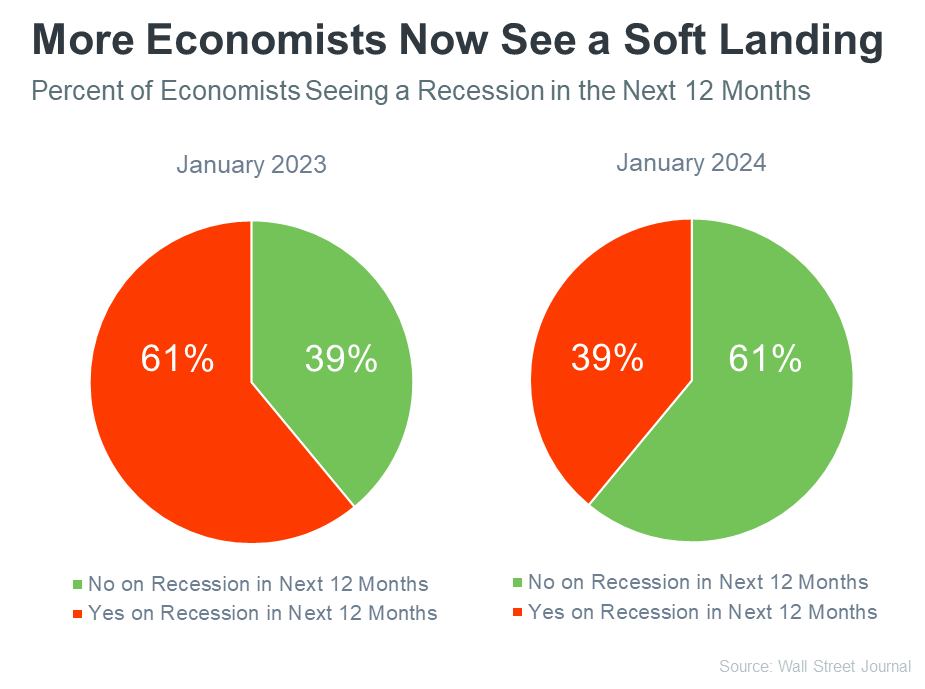

For all intents and purposes the economy is doing well. Economic data is showing continued growth (albeit with uncomfortable inflation) and low unemployment. This is helping to keep the recession narrative in check. In fact, as of January, only 39% of economists think there’ll be a recession in the next year. That’s way down from 61% projecting a recession just one year ago.

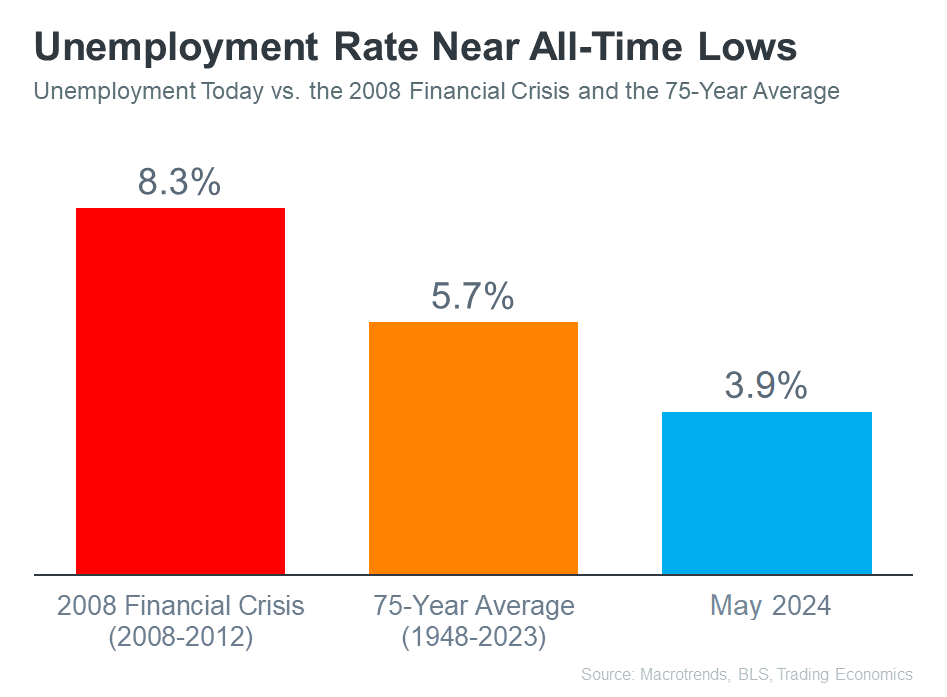

A big reason for economists’ recession view has to do with the unemployment rate. It’s currently near long-term lows at 3.9%.

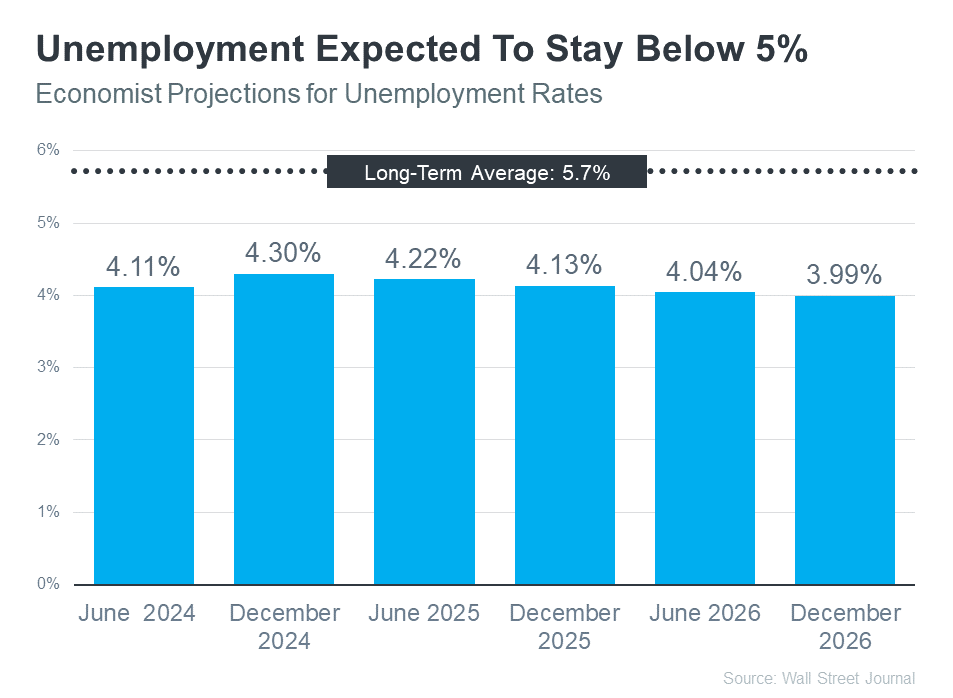

According to the Wall Street Journal experts are projecting the unemployment rate will remain below the long term average over the next few years.

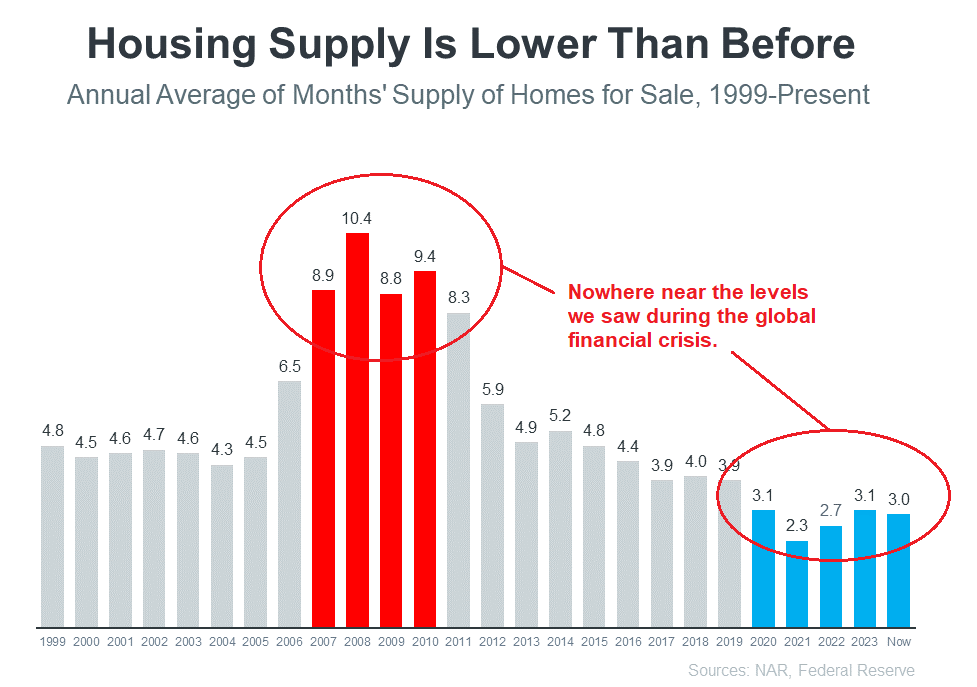

Let’s look at some data and trends specifically on the housing market. You’ll see that we are nowhere close to the conditions that existed prior to the global financial crisis and housing market crash of 2008-2009.

You’ve heard about the severe lack of housing inventory. Despite ramped up new home construction, we still have a shortage of homes for sale, and that’s keeping prices high. We currently have around a 3-month supply.

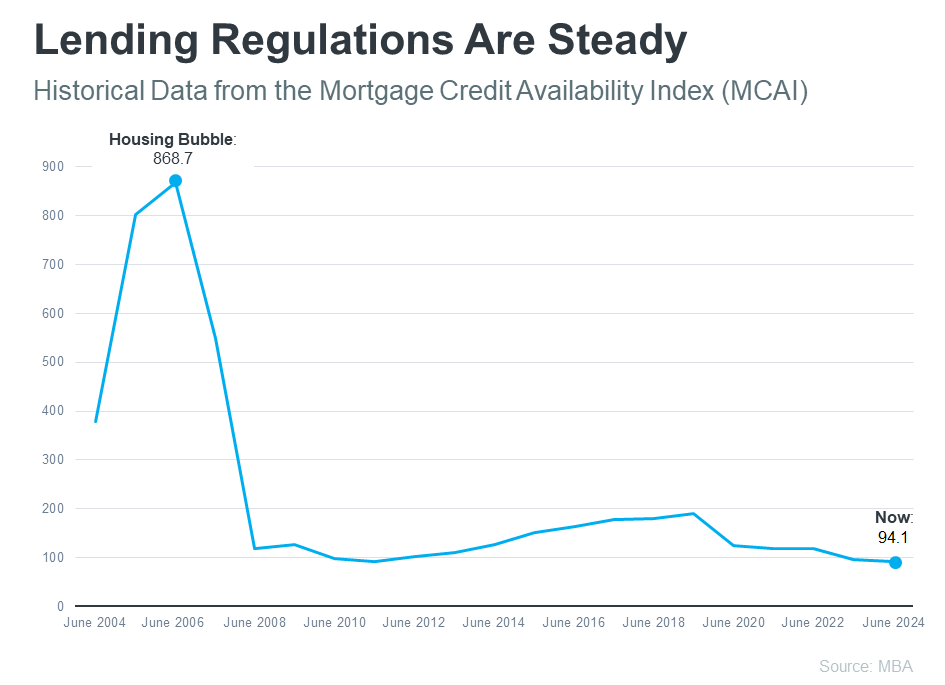

It’s harder to get a mortgage loan….and that’s actually a good thing. New rules and regulations that came out of the GFC ensure that the ultra-loose lending standards in place before the housing crash will not be repeated. Let’s take a look at the MCAI (Mortgage Credit Availability Index). The index indicates the relative difficulty or ease of getting a mortgage. A higher MCAI value suggests that credit is more readily available, while a lower value indicates that credit conditions are tighter. Notice how we are currently near index lows, which indicates tight lending conditions.

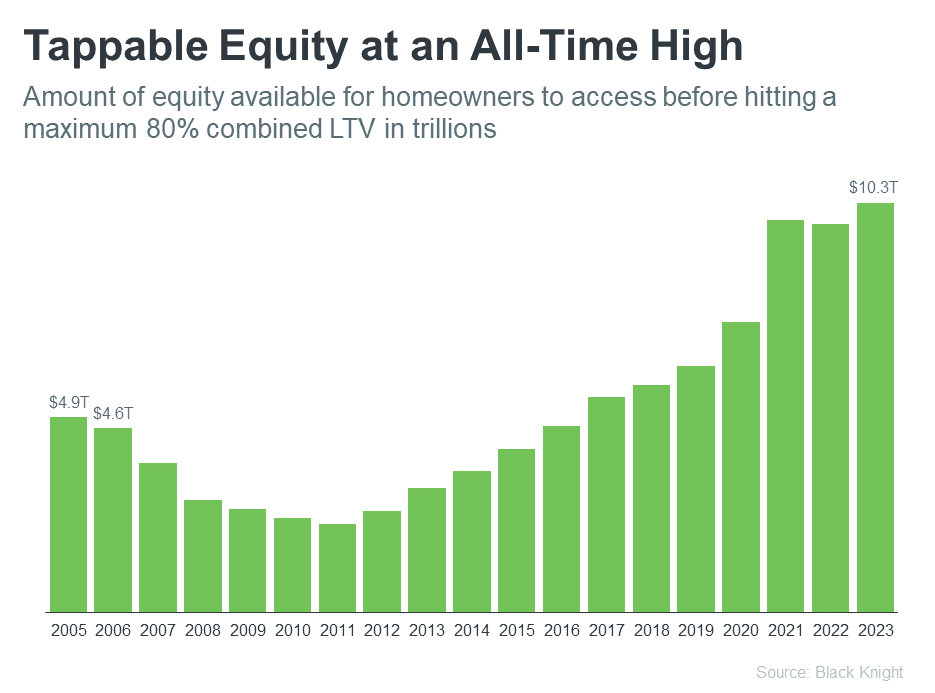

Current homeowners have the highest amount of tappable home equity in history….to the tune of $10.3T T=trillions!! This was not the case in the early 2000’s and it definitely exacerbated the 2008-2009 crash.

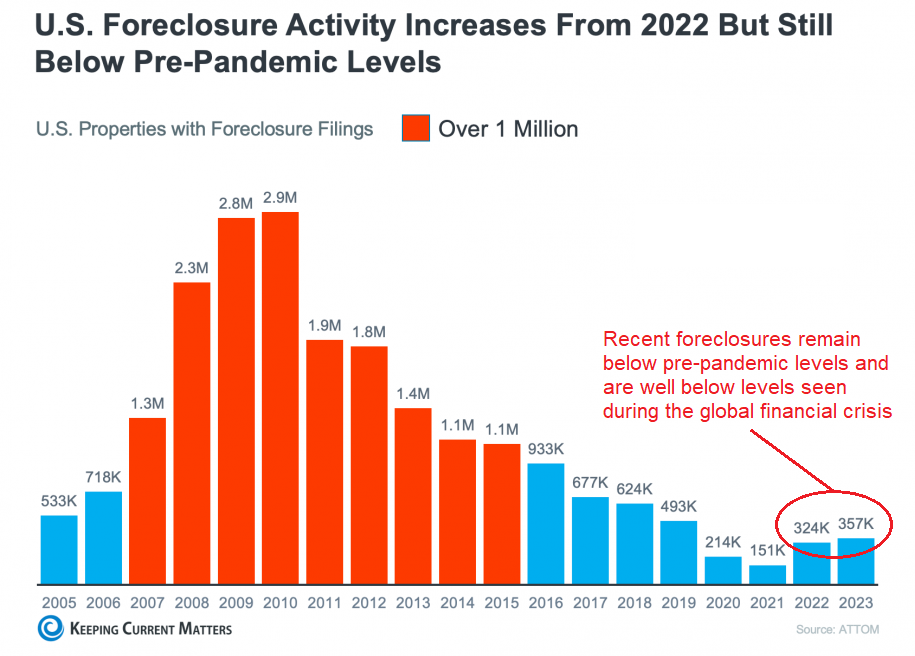

With so much home equity out there, foreclosure activity is low….very low, and this will help to keep home prices steady.

Considering the current economic and housing market conditions, it’s hard to build a case for a housing market crash. If you’re a prospective homebuyer, be careful when trying to time the market. If you’re waiting for home prices to crash, don’t hold your breath.