We’ve all been dealing with stubborn inflation for over a year now and just when you thought things were starting to get better, the second largest bank collapse in U.S. history unfolds (Silicon Valley bank – 3/10/23). Overseas in Switzerland we saw UBS takeover its crumbling rival Credit Suisse, pennies on the dollar (3/20/23). Let’s take a closer look at how this new banking crisis is affecting interest rates in general and what that means for prospective homebuyers and mortgage interest rates.

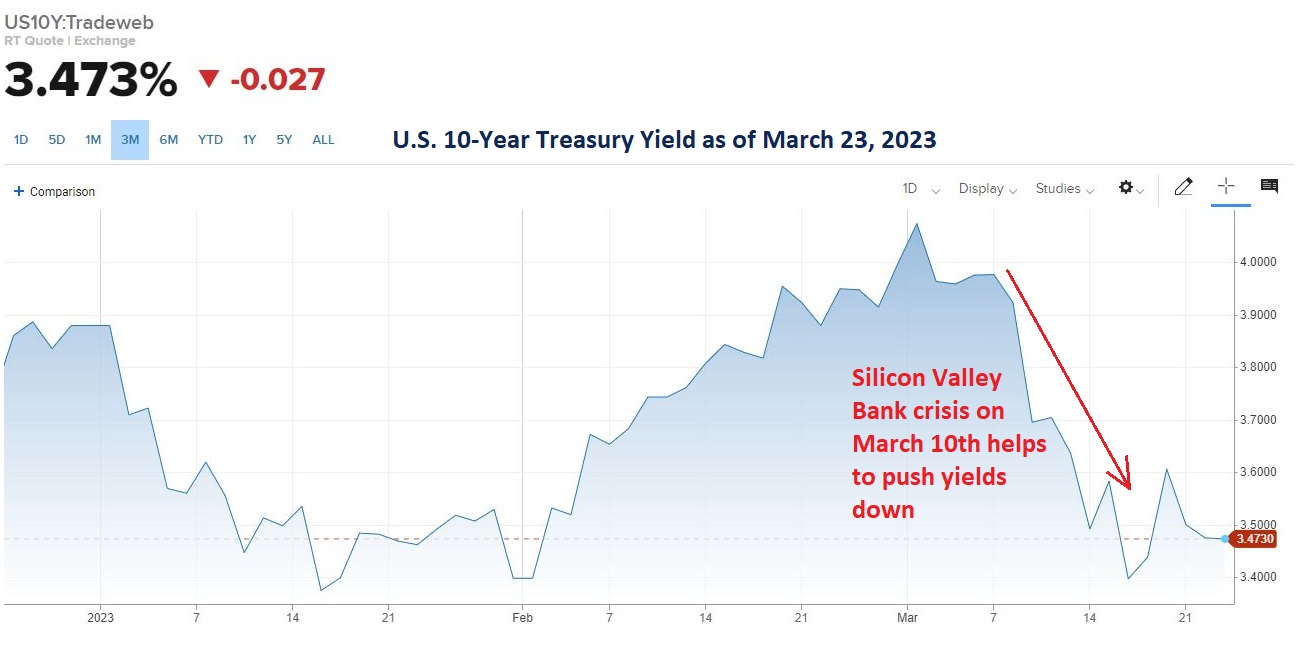

As you probably know, mortgage interest rates are tied very closely to the U.S. 10-yr Treasury Yield. Since the Federal Reserve started hiking interest rates in March of 2022, that yield has risen and so have mortgage interest rates. In fact, 30-yr fixed mortgage rates have breached 7% several times already, most recently earlier this month. But then the banking crisis happened and investors ran for cover and bought safe-haven U.S. Treasuries, forcing those yields back down.

Here’s that recent movement reflected in the 10-yr Yield:

While the banking crisis is an alarming event, there is a silver lining for homebuyers looking for a mortgage loan. As Treasury yields fall, mortgage rates typically follow. But guess what? Mortgage rates have come down a bit, but not nearly as much as the Treasury yields. Why? Because due to the banking crisis, credit is tightening. More on that later.

Here is a snapshot of average 30-yr mortgage rates as of 3/22/23:

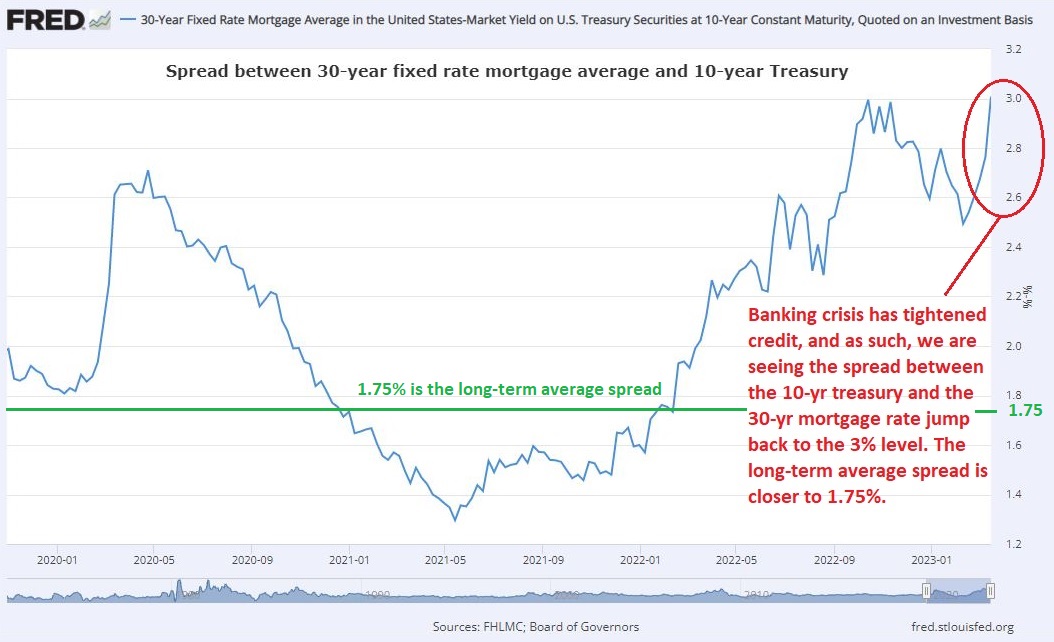

Tightening credit can be seen in the “spread” between the 10-yr yield and the 30-yr mortgage rate. Typically this spread is around 1.75%. In other words, if the 10-yr yield is 3.5%, then the corresponding 30-yr mortgage rate should be around 5.25%. But that’s not the case because of tightening credit conditions. Presently the “spread” is 3%, which would equate to a 6.5% 30-yr mortgage rate, and that’s exactly where we are today.

30-yr mortgage rate & 10-yr Treasure yield spread:

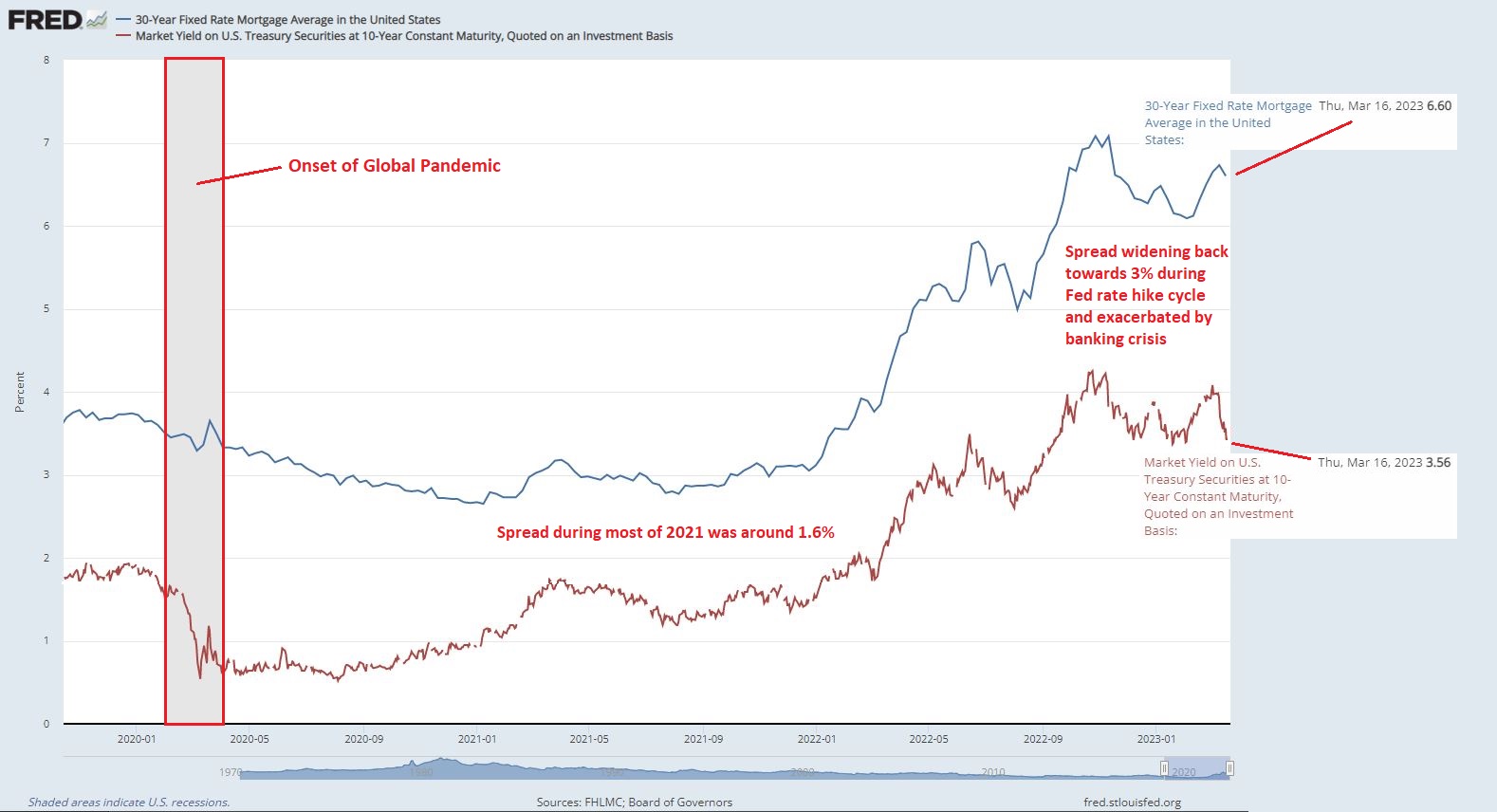

Here’s a chart of the 10-yr Treasury Yield and the 30-yr fixed mortgage rate from 2021 to present. Notice the correlation, but also take note of the “distance” between the two rates. This distance is the spread. Focus in on how wide the spread is over the last year or so (hovering close to 3%). This isn’t the norm. This extra wide spread is a reflection of uncertain times in the economy, A.K.A. tightening credit.

So what does this mean for prospective homebuyers going forward? Well…..Barring any additional banking crisis events, and assuming the Federal Reserve is nearing the end of its rate hike cycle, the spread should narrow back towards long-term averages. As the spread narrows, mortgage interest rates should trend lower. Time will tell the tale though. 😊

If any of the above is confusing, I’d be happy to discuss in further detail. Please feel free to reach out at your convenience by contacting me, or setting up a FREE Consultation.