Stubborn inflation and rising interest rates are on the minds of prospective homebuyers and for good reason. It’s considerably more expensive to finance a home now, than it was just a couple years ago. Seems very unfair, doesn’t it? But rents are up too…..up very much from pre-pandemic levels, and that’s making it difficult to save enough for a down payment. If you’re currently renting but looking to purchase a new home, here’s a handy tool that will help with your planning.

Our friends at MGIC (Mortgage Guaranty Insurance Corporation) have a great online calculator that quickly and easily shows consumers why it could make financial sense for them to invest in a home now rather than wait to save up a 20% down payment. Yes, if you don’t already know, you DO NOT need 20% down to purchase a house today. In fact, as a first time homebuyer, you may be able to put down as little as 3%!

So let’s run through a quick scenario, using the MGIC online calculator:

Assumptions:

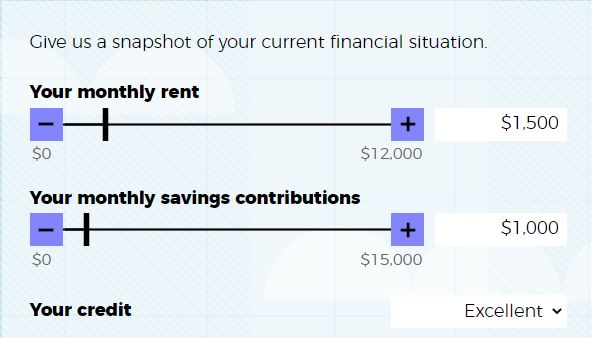

- Currently renting for $1500/mo

- Have $20k saved for a down payment

- Able to save $1000/mo towards the home purchase

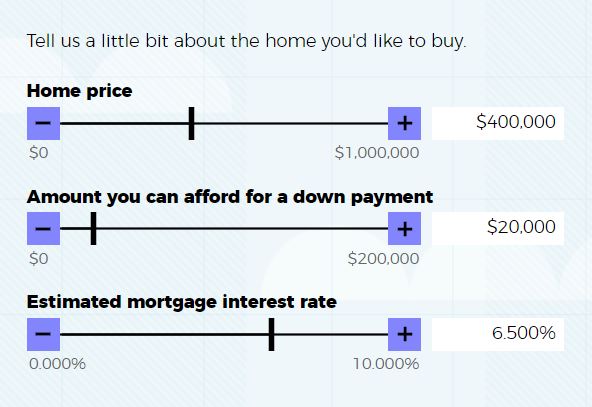

- Looking for a $400k home

Paying $1,500 per month for rent and saving $1,000 per month towards the new home.

Looking to purchase a $400k home, with $20,000 already saved for the down payment.

Current estimated 30-year fixed mortgage rates are around 6.5%.

Here are the results and some takeaways.

It will take over six years to be in a position to put 20% down. In the meantime, the landlord collects $123,588 in rent and you lose any chance of building home equity because you’re still renting. Consider this as well…..these days PMI (private mortgage insurance) isn’t horrible. For borrowers with good credit, your PMI monthly payment may not be nearly as expensive as you think, and with ALL CONVENTIONAL LOANS, PMI drops off automatically when you reach 78% LTV (Loan To Value). In the below example a borrower with excellent credit and 5% down will pay approximately $89/month for PMI. Not exactly a deal-killer, is it?

If you’d like to take the Buy Now vs. The Cost to Wait Calculator for a spin, please visit the MGIC website: Buy vs. Wait Mortgage Calculator: Explore the best time to buy a home (mgic.com)

If any of the above is confusing, I’d be happy to discuss in further detail. Please feel free to reach out at your convenience by contacting me, or setting up a FREE Consultation.