You don’t have to be a graduate student at MIT to know what’s happening in the economy. Runaway inflation is pushing the prices of everything up, and as a consequence, the Federal Reserve is hiking interest rates at an unprecedented pace. The resulting economic contraction typically creates a recession of some sort of magnitude. The question isn’t “if” but “when” we will slip into recession and how bad it will be. I’m not here to be part of that hotly debated topic, but rather to look back at past recessions to see how they affected the housing market.

First, let’s dispel some myths. Throughout Covid, the housing market saw incredible home price appreciation as buyers trampled over each other competing for historically low inventory amid record low interest rates. Post Covid, and during this cycle of rapidly increasing interest rates, you hear a lot of talk of 2023 being the next 2008 housing market meltdown. That’s just not going to happen and this is why, in a nutshell:

- There’s A Shortage Of Homes On The Market Today, Not A Surplus.

- Mortgage Standards Were Much More Relaxed Back Then.

- The Foreclosure Volume Is Nothing Like It Was During The Crash.

- The Global Pandemic Created An Unconventional Housing Market Landscape.

**For more detail on why we won’t see another 2008 meltdown, please see THIS BLOG POST

So with nearly two-thirds of economists predicting a recession in 2023, let’s take a look at the data and see what happened to the housing market in prior recessions.

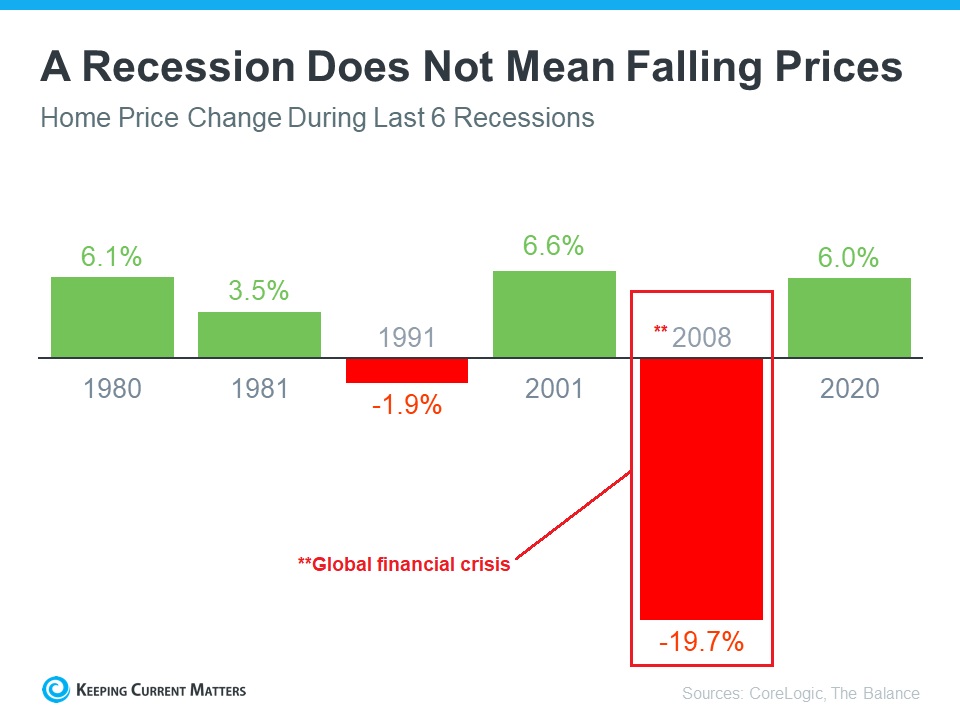

A Recession Doesn’t Mean Falling Home Prices

In the following chart, which includes the 2008 Global Financial Crisis you’ll notice housing prices in four of the last six recessions actually increased. Obviously, 2008 was a devastating outlier, but a plethora of new rules and regulations were enacted to ensure we do not see a repeat of that housing meltdown. If you don’t believe me, try applying for a “no-doc” or “stated income” mortgage loan 😉.

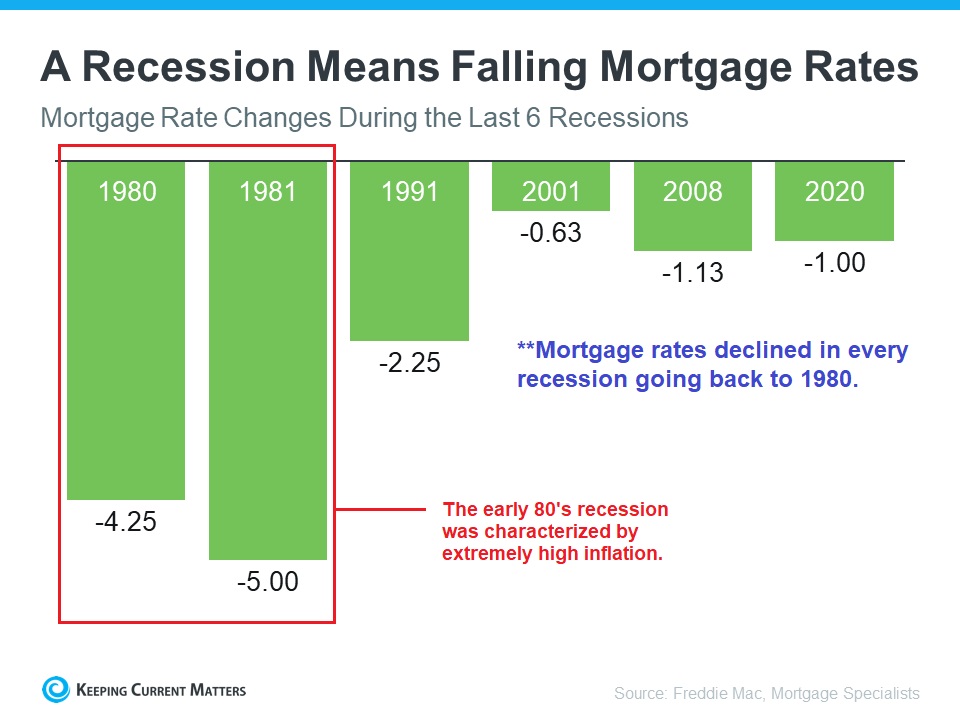

A Recession Means Falling Mortgage Rates

We are already seeing stabilizing mortgage interest rates even though the Federal Reserve has not officially signaled an end to their hiking cycle. This is potentially good news for homebuyers in 2023. History shows us that mortgage rates declined in every recession back to 1980 – also good news for future home buyers.

As a prospective homebuyer, you don’t necessarily have to worry about an upcoming recession, because history shows that it has a limited negative impact on the housing market. In fact, as long as you have the steady income and adequate credit required to finance a home, and you feel confident in your current employment, you should not put off homeownership. Think about it…..When the economy bounces back from the next recession, the housing market will react quickly, perhaps swinging the pendulum back in favor of the sellers. Remember those ugly bidding wars?